Materials Science

Is it a wrap for virgin plastics? 24th June 2019

By Sarah Harding, PhD

It has been estimated that 91% of all plastic ever produced has not been recycled. Sarah Harding takes a look at the current marke

It has been estimated that 91% of all plastic ever produced has not been recycled. Sarah Harding takes a look at the current market for recycled plastics, and some of the challenges and opportunities faced by this increasingly important sector.

Dubbed ‘the statistic of the year’, Great Britain’s Royal Statistical Society revealed in December 2018 the shocking fact that only about 9% of all plastic ever made has been recycled.1 Only 12% has been incinerated. The rest of it is in our landfills and oceans.

Since the vast majority of plastic is non-biodegradable, recycling is an increasingly important part of global efforts to reduce its presence in the waste stream. According to a recent MarketsandMarkets report,2 the global recycled plastics market was valued at $34.80 billion in 2016 – this was 2 years before the release of the final episode of the BBC’s Blue Planet II, which took an unflinching look at the impact of human activity on marine life, and rallied much of the Western world’s population behind Sir David Attenborough’s powerful call to protect the environment.

Another major development in the recycled plastic market was the ban on waste imports by China. On the first day of 2018, a huge shock hit the global recycling industry when China, then the world’s biggest scrap importer, stopped accepting virtually any recycled plastic from abroad. This affected the dynamic of the global recycled plastics market, leaving many developed countries to find new solutions for their growing piles of waste. The most logical way forward, for most of them, was to improve their own recycling systems, prompting them to re-use more recycled materials themselves.

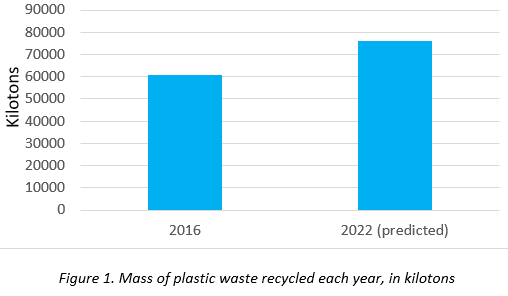

The recycled plastics market has been projected to reach $50.36 billion by 2022, at a CAGR of 6.4%.2 In terms of mass, this represents an 25% increase from 60,896 kilotons in 2016 to an expected 76,229 kilotons by 2022 (Figure 1). What might be considered a relatively slow annual growth, considering public and political pressures, probably reflects the technical difficulties currently experienced with the recycling process. The uptake of plastic recycling has been severely hindered by complexities of sorting and processing plastic waste. In particular, when different types of plastics are melted together, they tend to phase-separate (like oil and water), causing ‘phase boundaries’ that lead to structural weaknesses in the final material.

Recent innovations such as using block copolymers as ‘molecular stitches’ have been proposed to overcome these difficulties, and may increase the utility of recycled plastics in the future. Meanwhile, the percentage of plastics that can be fully recycled could be markedly increased if manufacturers were to minimize the mixing of materials and eliminate contaminants. To help with this effort, the Association of Plastics Recyclers has issued a Design Guide for Recyclability.3

The main plastics that are currently recycled are based on polyethylene terephthalate (PET), polyethylene (PE), polypropylene (PP), polyvinyl chloride (PVC) and polystyrene (PS). Although often limited by phase-separation – especially in the cases of PE and PP – recycled plastics have many applications in industries such as packaging, textiles, construction, automotive and electronics. Apparently, PET bottles are the largest and the fastest-growing source of recycled plastics.2 The majority of bottles are made of PET resins, which is the most commonly recycled resin and has the highest recycling rate in the plastics market. PET can be recovered and recycled repeatedly, and remoulded to produce new PET products. It can also be chemically broken into its constituent raw materials, which can then be purified and converted into new PET resins.

The negative environmental impact of using virgin plastics, growing consciousness of energy savings, and increasing applications across various industries are some of the major drivers of the recycled plastics market. In addition, world leaders across the globe have also come together to set ambitious targets for plastic recycling. For example, the European Commission has set a target for all plastic packaging on the EU market to be recyclable by 2030. Such targets are supported by national initiatives, such as the UK government’s declaration last year that, from April 2022, it plans to introduce a world-leading new tax on the production and import of plastic packaging with less than 30% recycled content.

Targets and initiatives surrounding plastic packaging might offer one reason why, according to Markets&Markets, packaging is the largest – and the fastest-growing – market for recycled plastics.2 This industry most commonly uses PET and HDPE resins, which are easily produced from recycling plastics. They possess various excellent properties such as strength, thermo-stability, and transparency, which makes them a popular choice for use in packaging. Recycled PET is used for packaging bottles for detergents and various other consumer products, and recycled HDPE for detergents, bleach, household chemicals and motor oil bottles.

So does all this mean that global demand for recycled plastics might soon see a sharp up-turn?

Well, maybe. With emerging new technologies for processing plastic waste, and improved infrastructures for sorting it, encouraged by government incentives across the globe and supported by public opinion… things are looking good for companies in the recycled plastics sector.

Some of the key players involved in plastics recycling include B&B Plastics (US), B Schoenberg & Co (US), Clear Path Recycling (US), Custom Polymers (US), Green Line Polymers (US), Jayplas (UK), KW Plastics (US), Suez (France) and Veolia Environnement (France).2 These companies are all involved in processing waste plastics and converting them into recycled resins which are then used in various applications. These companies have a strong foothold in global plastics recycling market, and it looks like business is good.

B Schoenberg & Co cries from its website that it has an “ONGOING NEED!!!” for source materials. “We consume 200 truckloads per month of flexible PVC scrap, regrind, parts or purge for use in our manufacturing plant,” they say. “Please call us immediately with any or all offers!”

KW Plastics makes a similar plea, saying “We’re not only the world’s largest plastics recycler, we’re also a plastic scrap buyer… Our vendors know they can depend on the KW Procurement Team for competitive market pricing, quality customer service, and reliable logistics.”

This apparent competition for plastic waste could lead you to believe that it’s becoming some kind of precious resource, in need by recycling companies struggling to keep up with demand for recycled plastic. One could even envisage a future where companies scavenge the oceans for waste, securing an important reserve while simultaneously clearing up the mess we’ve made of the planet. Yes, I’m probably getting ahead of myself there, but wouldn’t that be a wonderful solution to our current situation?

Because, as Sir Richard so memorably said, “The future of all life now depends on us.”

References:

- Parker L. National Geographic Society, 20th December 2018 (https://news.nationalgeographic.com).

- Markets & Markets. Recycled Plastic Market Report, April 2018 (https://www.marketsandmarkets.com/Market-Reports/recycled-plastic-market-115486722.html).

- Association of Plastics Recyclers. The APR Design® Guide for Plastics Recyclability, 2018 (www.PlasticsRecycling.org).

Author:

Sarah Harding worked as a medical writer and consultant in the pharmaceutical industry for 15 years, for the last 10 years of which she owned and ran her own medical communications agency that provided a range of services to blue-chip Pharma companies. In 2016, she began a new career in publishing as Editor of Speciality Chemicals Magazine, and in 2019 we were honoured to welcome her as Editorial Director at Chemicals Knowledge.

E: Sarah.Harding@ckhglobal.org